Home » Income Tax

Category Archives: Income Tax

NON-FILERS ALLOWED PURCHASE OF IMMOVABLE PROPERTIES, MOTOR VEHICLES

September 18, 2018.

Non-filers of income tax returns have been allowed to purchase immovable properties and motor vehicles as proposed on Tuesday through Finance Bill (Amendment) 2018/2019.

The non-filers were restricted in the budget 2018/2019 to purchase immovable property above Rs5 million and purchase of any engine capacity motor vehicles from Tax Year 2019 and onwards.

Finance Minister Asad Umar on the floor of house presented amendment to Finance Act 2018 and said that complained had been received from overseas Pakistani regarding difficulties in investing in immovable properties and purchase of motor vehicles due to restriction.

The finance minister said that overseas Pakistanis were mainly non-filers and considering the hardship faced by them it was decided to lift the condition.

The previous government through budget 2018/2019 imposed this restriction to increase the number of return filers for documentation of economy.

Finance Bill 2018: Immovable property, vehicle purchases only by return filers

The government has introduced major changes through Finance Bill 2018 for broadening the tax base and makes it mandatory purchases of immovable properties and vehicles only by filers of income tax returns.

A fundamental step has been taken in order to curb acquisition of certain assets by persons who are outside the taxation regime.

A new provision in the form of section 227C has been introduced which overrides any other law for the time being in force.

Under this provision, a person who is not a ‘filer’ (a taxpayer whose name does not appear in the active taxpayers’ list issued by the Board or is not holder of a taxpayer‘s card) will not be entitled to processing of any application:

- For booking, registration or purchase of a newly manufactured vehicle or imported vehicle.

- From any authority responsible for registration, recording, attesting immovable property.

This appropriate step which has been undertaken to curb the parking of untaxed money in acquisition of new vehicles and immovable properties need to be examined in the context of Constitutional provisions in relation to the fundamental right in respect of acquisition of assets.

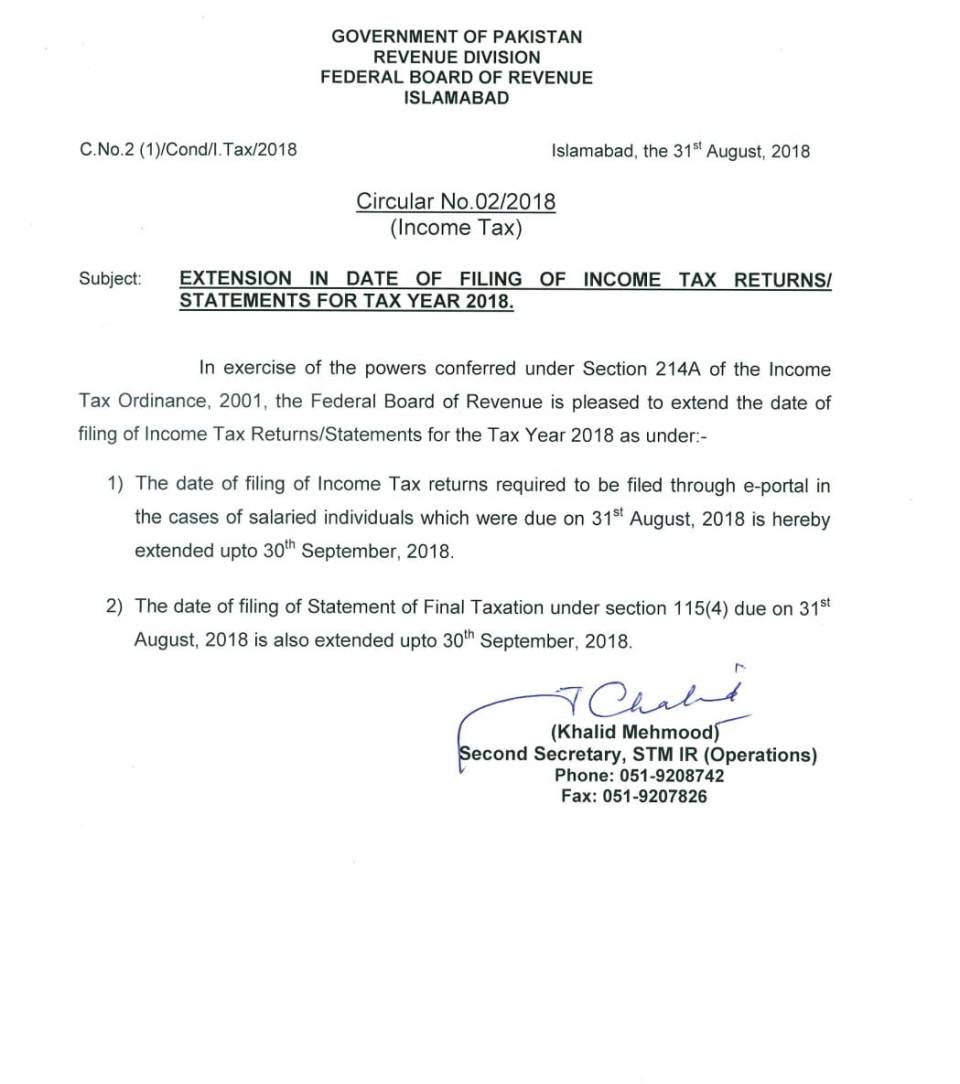

FBR extended the date of filing of Income Tax Return

FBR has extended the date of filing of Income Tax Return for salaried individual and Statement of final taxation u/s 115(4) for Tax Year 2018 up-to September 30, 2018.

Highlights of Finance Bill 2018

It explains following:

1. The Finance Bill 2018 includes certain policy changes in the taxation regime that have been there over three to four decades.

Following revolutionary positive measures have been introduced:

a) Valuation of Immovable Properties and the pre-emptive right of the Government to acquire under-declared properties;

b) Restriction on acquisition of immovable properties and new vehicles by nonfilers;

c) Measures relating to non-cash gifts between persons who are not relatives;

d) Abolition of presumptive tax regime for commercial Importers;

e) Introduction of the concept of year of discovery for taxation of unexplained foreign sourced income and foreign assets;

f) Withdrawal of immunity of foreign remittances exceeding certain threshold; and

g) Substantial reduction in tax rates for Individuals including salaried class.

2. As a result of the reduction in tax rates for businesses undertaken by Individuals, the difference in tax incidence for similar businesses undertaken by corporate sector and Association of Persons (AOP) vis-à-vis an Individual has widened.

The net effective take home income through a corporate business and AOP is limited to Rs 60 if the profit is Rs 100 whereas same business undertaken by an individual will result in take home income of Rs 85.

This difference may lead to de-corporatization of businesses. We propose that the gap should be reduced.

Generally accepted international measure for the same is to treat tax on dividend as adjustable against corporate tax liability so as to avoid economic double taxation.

3. The Government has introduced one time compliance scheme for disclosure of undeclared income and assets. The Finance Bill has proposed certain measures to curb the possibility of future accumulation of undeclared foreign assets and foreign income.

4. In order to incorporate tax measures for proper disclosure of foreign assets and foreign income and enhance the ambit of anti-avoidance provisions, the Finance Bill has introduced certain provisions which may deem a foreign source income as Pakistan source income.

This aspect needs to be examined in relation to the generally accepted principle of international taxation.

5. In order to avoid protracted litigation and delay in settlement of cases, the whole concept of Alternative Dispute Resolution (ADR) has been revamped.

Now, the ADR Committee (ADRC) will comprise of three members, out of which two will be independent persons.

If the taxpayer decides to opt for ADR regime instead of appellate regime then the recommendations of ADRC will be binding on both the parties.

6. In the past, certain anti-corporate tax measures such as levy of tax on bonus shares, tax on undistributed profits and super tax had been introduced.

Through the Finance Bill, corrective actions have been taken in respect of all these measures and tax on bonus shares has been abolished whereas the other two taxes are to be phased out over the period of time.

7. In the past, regressive measures were adopted that had rolled back the business oriented regime for group taxation.

It was expected that certain measures will be introduced to reinstate all-inclusive group taxation system.

No such measures are, however, appearing in the Finance Bill. It is expected that these measures will be taken care of in the Finance Act, 2018.

8. There has been disputes between taxpayers and tax department on the matter of taxability of composite contracts undertaken by non-residents.

These disputes inter alia primarily relate to taxation of offshore supplies being part of an overall arrangement.

The Finance Bill has proposed deeming provisions for taxation of income from such supplies which, in our view, overrides the principles of nexus as laid down in international taxation system.

This matter requires reconsideration to bring it in line with the generally accepted principles especially in the cases where the contracts are executed by a person resident in a tax treaty jurisdictions.

9. Domestic tax laws around the globe invariably provide principles to curb tax avoidance measures, however, details guidelines and processes are laid down for this purpose.

Substantial powers have been provided to taxation authorities for undertaking actions in case of tax avoidance schemes which include disregarding a legal entity and protection provided under the tax treaties.

These provisions without substantive guidelines and safeguards are prone to abuse by the tax authorities.

It is suggested that the application of the same be subject to the adoption of detailed guidelines for General Anti-Avoidance Regulations (GAAR).

10. Banking companies are subject to tax on their profits as determined by the regulations prescribed by State Bank of Pakistan (being the Regulator of Banking Sector in Pakistan).

The application of recharacterisation provisions in the case of banking companies is undesirable where the amount of profit is the one as determined in accordance with SBP regulations.

11. It should be the objective of every growth based taxation policy to encourage capital investment in plant and machinery.

This objective is achieved by allowing charge for depreciation against taxable income and the right to carry forward in subsequent year.

The Finance Bill has proposed certain measures whereby the right to adjust brought forward unabsorbed depreciation is being deferred.

This negates the very objective of the concept as described above which may lead to curtailment of industrial investment without any real benefit to the Government.

12. There has been a general and genuine complaint of taxpayers for repetitive selection for tax audits.

A corrective measure has been proposed whereby a composite audit, covering Income Tax, Sales Tax and Federal Excise, shall be undertaken not more than once in three years.

There are cases of abuse of provisions relating to amendment of assessment in order to create tax demands. Corrective measures are required in this regard also.

Mobile Handset Levy

A new levy on mobile handsets is all set to stir things up come July 1st. It is called the Mobile Handset Levy, and the government is expecting to collect around Rs. 12 billion revenue from it. The levy is fashioned after a similar exercise run in different countries.

It involves matching the IMEI numbers of all legally imported handsets with those that are active on the networks of telecom operators on a daily basis. If an IMEI number is on the network but its record does not exist with the Federal Bureau of Revenue (FBR), an automatic SMS will be sent to that device asking the owner to deposit sales tax, customs duty as well as the handset levy with the tax authorities within 30 days. Failure to comply will result in the device being barred from all Pakistani networks.

The amount of the levy varies, depending on the cost of the device. All devices below Rs 10,000 will be exempt. Those that cost between Rs 10,000 and Rs. 40,000 will charged Rs 1,000 as handset levy while those between Rs 40,000 and 80,000 will be charged Rs 3,000. Finally, the handsets whose cost is above Rs 80,000 will be will be levied a payment of Rs 5,000.

| Cost of the device |

Amount of the levy |

| Below Rs. 10,000 | Exempt |

| From Rs. 10,000 to 40,000 | Rs. 1,000 |

| From Rs. 40,000 to 80,000 | Rs. 3,000 |

| Above Rs. 80,000 | Rs. 5,000 |

Sources in the finance ministry tell Dawn that an exercise is currently underway to enable data sharing between the Pakistan Telecommunications Authority (PTA) and the FBR. All legally imported mobile handsets have their IMEI numbers registered with the customs authorities at the time duties and sales taxes are paid, giving FBR a database of all such handsets. However, the IMEI number of all smuggled handsets doesn’t exists in the FBR database. The new program will compile a daily database of the IMEI numbers of all handsets that are connected to Pakistani networks. Those devices whose IMEI number has no record in the FBR database will automatically be flagged as a smuggled device, and the owner will be required to pay the duties and taxes in addition to the handset levy, to continue using their device.

Sources reveal to Dawn that several meetings to create this number-matching system have already been held, and the PTA is preparing to do a soft launch of the program on May 25, which hopes to iron out all glitches till June 30 after which the system will be launched. To process the payment, the government has built a system that will enable users to pay online or through an ATM machine, the sources add.

Most people do not know whether the device they are using is legally imported, with all duties and sales tax paid, or it is smuggled with tax and duty evaded. According to government figures, around 10 million handsets are imported into the country legally every year and 8.2m have already been imported so far till March 2018. There is no data available on the size of smuggled handsets.

The finance minister says the levy is designed to discourage smuggling of handsets, as well as promoting registration of all IMEI numbers, that can help curb mobile phone theft. “Through this system,” he tells Dawn, “we can ensure that a stolen phone will never be able to connect to a Pakistani network again.” He also hopes it will encourage local assembly of handsets

Source: https://www.dawn.com/news/1404525

Salient Features of Taxes applied on Real Estate Sector

- Property Transactions shall be recorded at the value declared by the buyer and the seller of the Property.

- Property Rates notified by FBR (for the purpose of collection of taxes on sale / purchase of property) and DC rates are to be abolished.

- At the Federal level, a one percent adjustable advance tax from the purchaser on the declared value shall be collected and this tax shall replace the existing withholding tax on sellers and purchasers of Property.

- Non-filers shall not be permitted to purchase property having declared value exceeding Rs. 4,000,000/- (four million rupees).

- Provinces shall be reque

sted to abolish the provincial rates for the collection of stamp duty (commonly known as DC rates) and to collect a total of one percent tax under stamp duty and capital value tax on the value declared by the buyer and the seller of property.

sted to abolish the provincial rates for the collection of stamp duty (commonly known as DC rates) and to collect a total of one percent tax under stamp duty and capital value tax on the value declared by the buyer and the seller of property. - In order to deter under-declaration and consequent loss of revenue, FBR shall have the right to purchase any property within six months of registration by paying a certain amount over and above the declared value which may be 100 percent in the fiscal year 2018-19, 75 percent in the fiscal year 2019-20 and 50 percent in the fiscal year 2020-21 and thereafter.

How to wind up a company?

How to wind up a company? It is a very important question which a professional must know the answer of.

I am sharing here some useful guide for the procedure and legal requirements to wind up a company. I hope that it will be equally useful for the professionals and students of Chartered Accountancy.

The term ‘winding up’ of a company may be defined as the proceedings by which a company is dissolved (i.e. the life of a company is put to an end). Thus, the winding up is the process of putting an end to the life of the company. And during this process, the assets of the company are disposed of, the debts of the company are paid off out of the realized assets or from the contributories and if any surplus is left, it is distributed among the members in proportion to their shareholding in the company. The winding up of the company is also called the ‘liquidation’ of the company. The process of winding up begins after the Court passes the order for winding up or a resolution is passed for voluntary winding up. The company is dissolved after completion of the winding up proceedings. On the dissolution, the company ceases to exist. So, the legal procedure by which the existence of an incorporated company is brought to an end is known as winding up.

Modes of winding up

Modes of winding up

The winding up of a company may be either-

(i) by the Court; or

(ii) voluntary; or

(iii) subject to the supervision of the Court

- PROCEDURE FOR WINDING UP OF COMPANY AND FILING OF PETITION BEFORE RESPECTIVE HIGH COURT:

-

- To pass Special Resolution by 3/4th majority of the members of the company

that the company be wound up by the Court in case if the company itself intend

to file a petition and to file the Special Resolution on Form 26 with the

registrar. - To prepare a list of the assets to ascertain that the company is unable to pay its

debts. - To prepare a list of the creditors

- In case of defaults in payments the creditor or creditors to make a decision for

the filing of the winding up petition. - In case if the Commission or Registrar or a person authorised by the

Commission intend to file a petition, they should not file a petition, for winding

up of the company, unless an investigation into the affairs of the company has

revealed that it was formed for any fraudulent or unlawful purpose or that it is

carrying on a business not authorised by its memorandum or that its business is

is

being conducted in a manner oppressive to any of its management has been

guilty of fraud, misfeasance or other misconduct towards the company or

towards any of its members. - To engage advocates for the preparation and filing of the petition.

- To pass Special Resolution by 3/4th majority of the members of the company

- PROCEDURE FOR VOLUNTARY WINDING UP

The following steps are to be taken for Member’s voluntary winding up under the Provisions of the Ordinance, and the Companies Rules.

Step 1. Where it is proposed to wind up a company voluntarily, its directors make a declaration of solvency on Form 107 prescribed under Rule 269 of the Rules duly supported by an auditors report and make a decision in their meeting that the proposal to this effect may be submitted to the shareholders. They, then, call a general meeting (Annual or Extra Ordinary) of the members (Section 362 of the Ordinance)

Step 2. The company, on the recommendations of directors, decides that the company be wound up voluntarily and passes a Special Resolution, in general meeting (Annual or Extra Ordinary) appoints a liquidator and fixes his remuneration. On the appointment of liquidator, the Board of directors ceases to exist. (Sections 358 and 364 of the Ordinance)

Step 3. Notice of resolution shall be notified in official Gazette within 10 days and also published in the newspapers simultaneously. A copy of it is to be filed with registrar also. (Section 361 of the Ordinance)

Step 4. Notice of appointment or change of liquidator is to be given to registrar by the company alongwith his consent within 10 days of the event. (Section 366 of the Ordinance)

Step 5. Every liquidator shall, within fourteen days of his appointment, publish in the official Gazette, and deliver to the registrar for registration, a notice of his appointment under section 389 of the Ordinance on Form 110 prescribed under Rule 271 of the Rules.

Step 6. If liquidator feels that full claims of the creditors cannot be met, he must call a meeting of creditors and place before them a statement of assets and liabilities. (Section 368 of the Ordinance)

Step 7. A return of convening the creditors meeting together with the notice of meeting etc. shall be filed by the liquidator with the registrar, within 10 days of the date of meeting. (Section 368 of the Ordinance)

Step 8. If the winding up continues beyond one year, the liquidator should summon a general meeting at the end of each year and make an application to the Court seeking extension of time. (Section 387(5) of the Ordinance)

Step 9. A return of convening of each general meeting together with a copy of the notice, accounts statement and minutes of meeting should be filed with the registrar within 10 days of the date of meeting. (Section 369 of the Ordinance)

Step 10. As soon as affairs of the company are fully wound up, the liquidator shall make a report and account of winding up, call a final meeting of members, notice of convening of final meeting on Form 111 prescribed under Rule 279 of the Rules before which the report / accounts shall be placed. (Section 370 of the Ordinance)

Step 11. A notice of such meeting shall be published in the Gazette and newspapers at least10 days before the date of meeting. (Section 370 of the Ordinance).

Step 12. Within a week after the meeting, the liquidator shall send to the registrar a copy of the report and accounts on Form 112 prescribed under Rule 279 of the Rules. (Section 370 of the Ordinance)

- PROCEDURE FOR CREDITOR’S VOLUNTARY WINDING UP

Step 1. First of all, the company passes a special resolution in the general

meeting of the members of the company for which following steps are to taken:

- Board of Directors approves the agenda of the general meeting especially the draft special resolution for winding up of the company.

·Notice of the general meeting alongwith copy of the draft special resolution is given to the members at least 21 days before the general meeting.

·Special resolution is passed by 3/4th majority of the members of the company and the members appoint a person to be liquidator of the company.

·Special resolution on Form 26 is filed with the registrar.

Step 2 . Meeting of creditors is called at 21 days notice, (simultaneously with sending of the notices of the general meeting of the company) the notice of the meeting of the creditors to be send by post to the creditors, besides, the notice of the said meeting to be advertised in the official Gazette and the newspaper circulated in the Province and the creditors pass a resolution of voluntary winding up of the company. The creditors also appoint liquidator in that meeting. If the creditors and the company nomina te different persons, than person nominated by the creditors shall be liquidator.

Step 3. Notice of the resolution passed at the creditor’s meeting shall be

given by the company to the registrar alongwith consent of the liquidator within ten

days of the passing of the resolution.

The company may either at the meeting at which resolution for voluntary winding

up is passed or at any subsequent meeting may, if they think fit, appoint a committee of inspection consisting of not more than five persons. Provided that the creditors may, if they think fit, resolve that all or any of the person so appointed by the company ought not to be member of the committee of inspection.

Step 4. The liquidator should, with all convenient speed, realise the assets, prepare lists of creditors, admit proof, settle list of contributories, make such calls as may be necessary, etc. accordingly as the nature of the case may require, pay secured creditors, pay the costs including the liquidator’s own remuneration, pay preferential claims, and after meeting all the claims of creditors, and after adjusting all claims and rights, distribute the surplus on pro rata basis.

Step 5. In the event of the winding up continuing for more than one year, the liquidator shall summon a general meeting of the company and a meeting of creditors at the end of the first year from the commencement of the winding up and lay before the meetings an audited account of receipts and payments and acts and dealings and of the conduct of winding up during the preceding year together with a statement in the prescribed form and containing the prescribed particulars with respect to the proceedings and position of liquidation and forward by post to every creditor and contributory a copy of the account and statement together with the auditors’ report and notice of the meeting at least ten days before the meeting required to be held.

Step 6. The liquidator prepares the accounts, gets them audited and also presents a final report to the creditors. The steps at this stage are as under:

·The liquidator prepares a final report and accounts of the winding up, showing how the winding up has been conducted and the property of the company have been disposed of.

·Accounts are duly audited by the auditor appointed for the purpose.

·The notice of meeting is sent by post to each contributory of the company and creditor at least ten days before the meeting. The account with a copy of the auditor’s report is also enclosed with the notice.

·The notice of the meeting specifying the time, place and object of the meeting is published at least ten days before the date of the meeting in the official Gazette and in at least one newspaper.

·Within one week after the meeting, the liquidator is required to send to the registrar a copy of his report and account, and make a return to him of the holding of the meeting alongwith the minutes of the meeting.

·If a quorum is not present at the meeting, the liquidator makes a return stating that the meeting was duly summoned and that no quorum was present thereat. The return is filed with the registrar and considered as presented in the meeting.

·The registrar, on receiving the report, account and the return, is required to register them after their scrutiny.

·On the expiration of three months from the registration of final report, accounts and minutes, the company is deemed to be dissolved

- For more details please see

SECP guide on winding up

Alternative Corporate Tax

Introduction to ACT :

– A new section 113C titled as “Alternative Corporate Tax” has been introduced through Finance Act, 2014, which starts with a “non-obstante clause” i.e. Notwithstanding anything contained in this Ordinance (Income Tax Ordinance, 2001)

– Applicable for tax year 2014 and onwards

– Tax payable by a “Company” will be higher of the “Corporate Tax” (generally includes minimum and final taxes apart from certain exceptions) or “Alternative Corporate Tax” (17% of Accounting Income subject to certain adjustments and exclusions)

– Rationale for introduction of ACT was explained in the “Salient features” of Budget documents “to discourage perpetual declaration of losses or very low income using tax avoidance means by Companies”.

– The Finance Minister in his Budget Speech also mentioned that “ACT is being introduced for corporate cases where taxable income is usually far less than accounting income due to careful tax planning to avail all possible avenues of tax avoidance technically.”

International Examples :

– India

18.5% of book profits of the Company (termed as adjusted accounting profits).

– Argentina

Applicable at 1% of the value of fixed and current assets.

– Mexico

17.5% of Flat Tax Base computed on the basis of certain cash inflows and outflows

– Austria

Minimum amounts of tax have been prescribed for certain types of companies.

– Mauritius

7.5% of book profits or 10% of dividends, whichever is higher.

Except for Mauritius, in all the above cases, adjustment is allowed for next 10 years.

Effect of non-obstante clause :

– The provisions of section 113C only have an overriding effect over other provisions of the Income Tax Ordinance, 2001

– In case of any conflict between the provisions of section 113C and any other provision of the Income Tax Ordinance, 2001, the provisions of section 113C will prevail

– If, however, there is a conflict between section 113C and any other provision of a Special Statute, the provisions of section 113C will remain subservient to the provisions of such Special Statute. Much would, however, depend upon the language of such Special Statute and the nature of conflict.

– The provisions of section 113C are in the nature of “Self Contained code”. Other provisions of the Income Tax Ordinance cannot be applied automatically except to the extent permitted by Section 113C itself.

Effective year & retrospective application :

– Specifically mentioned to be applicable for tax year 2014 and onwards.

– Not a one-time levy but also intended to be applicable for subsequent tax years.

– Companies following Special Tax Years already ended before introduction of section 113C are affected by this levy.

– Even for Companies following June 30 as their year-end are also affected by this law as all advance tax payments were already made in accordance with normal provisions.

– ACT, thus, has a retrospective effect for tax year 2014 by way of expressed language and not by way of any intendment.

– Constitutional validity of the retrospective application is to be decided by the Courts. It is, however, generally believed that a retrospective law is valid if made through expressed legislation.

Taxpayers covered by ACT :

– ACT is only applicable on a “Company” and as such, all other categories of taxpayers, such as Individuals and Association of Persons are not covered.

– Unlike section 113, ACT is also applicable on non-resident companies.

– Section 113C itself does not define the term “Company” and, therefore, the term has to be construed as per section 80 to include the following.

(a) Locally incorporated Companies, body corporates, Small Companies

(b) Modarabas

(c) Foreign companies

(d) Co-operative societies, Finance societies and other societies

(e) Non-profit organisations

(f) Trust, an entity or body of persons established or constituted by any law

(g) Foreign associations declared by FBR as a Companies

(h) Provincial Governments

(i) Local Governments in Pakistan

Companies not covered by ACT :

– ACT is specified to be non applicable on Taxpayers chargeable to tax in accordance with the following provisions of Income Tax Ordinance, 2001

(a) Fourth Schedule (Insurance Companies)

(b) Fifth Schedule (Mining Companies)

(c) Seventh Schedule (Banking Companies)

– By implication, ACT is also not applicable on following companies:

(i) Companies setting up an Industrial Undertaking between July 1, 2014 to June 30, 2017 and subject to certain conditions, eligible for a reduced tax rate of 20% for a period of five years

(ii) Non-profit organisations and certain trusts and welfare institutions eligible for 100% tax credit under section 100C

(iii) Companies eligible for 100% tax credit under section 65D not having any other income

(iv) Companies not deriving any income other than exempt or certain incomes subject to final taxation or Capital Gains under section 37A

(v) Non-resident companies not having any presence in Pakistan

Computation of ACT :

– ACT is defined as the tax at a rate of 17% of a sum equal to “Accounting Income” as reduced by certain specific adjustments.

– “Accounting Income” is defined as the accounting profit before tax for the tax year, as disclosed in the financial statements, excluding share from the associate recognised under equity method of accounting.

– Following amounts are also excluded from accounting income for computing ACT.

(a) exempt income

(b) income subject to tax under section 37A (capital gains on securities)

(c) income subject to final taxation under section 148(7) – Imports, Section 150 (Dividends), Section 153(3) – Resident Suppliers and Contractors, Section 154 (Exports), Section 156 (Prizes & winnings) and section 233 (3) – Brokerage and Commission

(d) income subject to tax credit under sections 65D and 65E (equity investment in certain Industrial Undertakings)

(e) income subject to tax credit under section 100C (NPOs and certain trusts & welfare institutions); and

(f) income of the Company subject to reduced rate of tax under newly inserted clause 18A of Part II of the Second Schedule

– The sum equal to accounting income less any amount to be excluded therefrom (as mentioned in (a) to (f) above) is to be treated as “Taxable income” for the purposes of section 113C.

– For the purposes of determining the “Accounting Income”, expenses are required to be apportioned between the “excluded amounts” and the balance accounting income (being treated as “taxable income”). FBR’s Circular suggests the apportionment on turnover basis.

– The Commissioner is empowered to make adjustments and proceed to compute accounting income as per historical accounting pattern after providing an opportunity of being heard.

– Tax credit under section 65B (on investment in BMR Plant & Machinery) is allowed against ACT.

Corporate Tax :

Defined as total tax payable by the Company, including-

- tax payable on account of minimum tax (e.g. Minimum tax on turnover under section 113, Minimum tax on builders under section 113A, Minimum tax on land developers under section 113B, minimum tax under section 148(8) on importers of edible oil and packing material, minimum tax under clauses 56B, to 56G for certain persons opting to be taxed under normal tax regime)

- final taxes payable under any provision of the Ordinance but not including those mentioned in Section 8 (FTS and royalty of non-resident persons not having Permanent Establishments in Pakistan, incomes of non-resident shipping & airlines, dividend income)

Following taxes are excluded:

– Section 161 (tax recovered from payer due to default in withholding tax compliance)

– Section 162 (tax recovered from the recipient due to withholding tax non- compliance of payer)

– Default Surcharge or penalty

– ACT payable under section 113C

Carry forward of ACT :

– The excess of Alternative Corporate Tax paid over the Corporate Tax payable for the tax year is to be carried forward and adjusted against the tax payable under Division II of Part I of the First Schedule for following year.

– If the excess tax is not wholly adjusted the unadjusted amount is to be carried forward to the following tax year and so on, however, the excess cannot be carried forward to more than ten tax years immediately succeeding the tax year for which the excess was first computed.

– The entitlement to carry forward minimum tax under section 113 will remain unaffected by ACT.

– If Corporate Tax or ACT is enhanced or reduced as a result of any amendment or as a result of any order, the excess amount to be carried forward will be adjusted accordingly.

FBR’s computational examples :

Example 1 – Explanation of carried forward minimum tax & ACT

Example 1 – Explanation of carried forward minimum tax & ACT

| Corporate Tax (excluding minimum tax) | (A) Rs 100 |

| Minimum tax under section 113 | (B) Rs 140 |

| ACT | (C) Rs 200 |

| Corporate Tax under section 113C | (D=A+B) Rs 140 |

| Excess amount of ACT over Corporate Tax carried forward for next ten tax years | (C-D) 60 |

| Excess amount of Minimum tax carried forward for next five years | (B-A) 40 |

– Discriminatory to Corporate Sector which is documented and subject to Corporate Regulatory requirements whereas other taxpayers such as sole proprietors and AOPs are not subject to ACT regime. The possibility of extending ACT to other taxpayers cannot be ruled out.

– The provision penalises the so-called low tax / no tax paying companies by ignoring the overall contribution to the economic development and omitting to take into account the effect of contribution to the Exchequer by way of other indirect taxes, such as Sales Tax, Provincial Sales Tax, FED and Customs Duty, etc.

– The rationale for 17% of accounting profit is not known and there is no surety if the rate of ACT will remain static in future years depending upon the revenue pressures.

– Arbitrary powers of the Commissioner to determine the accounting profit especially with regard to the unclear terms “historical accounting pattern” and “profit before tax for the tax year as disclosed in the financial

statements.”

PwC 18

– Lack of clarity on the basis of computing excluded items such as exempt income.

– No rationale for apportionment of all expenses especially when there are identifiable direct expenses and the Company is liable to WWF and WPPF.

– Treatment of non-taxable items (such as capital receipts / gain on sale of immovable property held for more than 2 years / 25% of capital gains on long term assets).

– No tax credit other than section 65B will be allowed against ACT, such as Charitable donations (under section 61), sales to registered persons (section 65A) and enlistment (65C).

– Likely to have an impact for small companies entitled to be taxed at a reduced rate of 25% under normal basis.

PwC 19

– Companies having brought forward tax losses and unabsorbed depreciation may also be affected by ACT, which is only applicable on accounting profit for the tax year without any impact of brought forward losses and unabsorbed depreciation

– Following classes of income and persons (otherwise covered by FTR) have not been

excluded from Accounting Income:

(a) Import of ships by ship breakers

(b) Non-resident contractors opting for taxation under FTR

(c) Commission / discount of petrol pump operators

(d) Income of a CNG station

(e) Shipping business qualifying for reduced rate on tonnage basis as final tax

(f) Income from services rendered and construction contracts outside Pakistan subject to tax at 1% of gross receipts

– Adjustment of ACT against taxes payable under the above categories is not provided

PwC 20

– No consequential amendment has been made in section 147 thereby creating an ambiguity as regards the payment of ACT by way of advance tax

– Likely mismatch between the income taxable under FTR (generally on receipt basis)

with the corresponding amounts disclosed in financial statements (on accrual basis)

– Application of ACT on companies opted for group taxation as single fiscal unit

– Treatment of remittance of after tax profits by branches of non-resident companies deemed as dividend requires clarity as the same does not form part of accounting income before tax