Home » 2016 (Page 3)

Yearly Archives: 2016

JOINT AND SEVERAL LIABILITY OF REGISTERED PERSONS IN SUPPLY CHAIN WHERE TAX UNPAID (SEC-8B)

JOINT AND SEVERAL LIABILITY OF REGISTERED PERSONS IN SUPPLY CHAIN WHERE TAX UNPAID (SEC-8B)

_ Where a registered person receiving a taxable supply from another registered person is in the knowledge or has reasonable grounds to suspect that some or all of the tax payable in respect of that supply or any previous or subsequent supply of the goods supplied would go unpaid of which burden to prove shall be on the department, such person as well as the person making the taxable supply shall be jointly and severally liable for payment of such unpaid amount of tax.

_ Provided that the Board may by notification in the official gazette, exempt any transaction or transactions from the provisions of this section.

COLLECTION OF EXCESS SALES TAX (SEC-3 B)

COLLECTION OF EXCESS SALES TAX (SEC-3 B)

_ Any person who has collected or collects any tax or charge, whether under misapprehension of any provision of this Act or otherwise, which was not payable as tax or charge or which is in excess of the tax or charge actually payable and the incidence of which has been passed on to the consumer, shall pay the amount of tax or charge so collected to the Federal Government.

_ Any amount payable to the Federal Government shall be deemed to be an arrears of tax or charge payable under this Act and shall be recoverable accordingly and no claim for refund in respect of such amount shall be admissible.

_ The burden of proof that the incidence of tax or charge has been or has not been passed to the consumer shall be on the person collecting the tax or charge.

| Exercise :

Hassan (Pvt.) Ltd. under misapprehension collected additional sales tax of Rs. 100,000 from one of its customers. 65% of the goods on which additional sales tax was collected are still lying with the customer as unsold stock. |

| Answer :

In the above scenario, since 65% of the stock, on which excess tax of (100,000 x 65%) Rs. 65,000 was collected, is still unsold, Hassan Ltd should return this amount to its customer. However, the balance amount of Rs. 35,000, the incidence of which has been passed on to the consumers should be deposited with the Federal Government. |

WHO IS LIABLE TO PAY SALES TAX ?

LIABILITY TO PAY SALES TAX

The liability to pay the tax shall be:

(i) In the case of supply of goods in Pakistan, of the person making the supply, and

(ii) In the case of goods imported into Pakistan, of the person importing the goods.The Federal Government may specify the goods in respect of which the liability to pay tax shall be of the person receiving the supply.

SCOPE OF SALES TAX

WHAT IS THE SCOPE OF SALES TAX ?

It is very important question for a person studying SALES TAX ACT 1990, either for practice or for preparation of Examinations. Here we are going to share with you the scope of SALES TAX in Pakistan in nutshell.

Hope it will be helpful for you both in examinations and practice.

Normal rate of sales tax

– Sales tax @ 17% is charged, levied and paid on the value of:

(i) taxable supplies made by a registered person in the course or furtherance of any taxable activity carried on by him; and

(ii) goods imported into Pakistan.

– Where the taxable supplies are made to a person who has not obtained registration number, there shall be charged, levied and paid a further tax at the rate of 2% of the value in addition to the normal rate of 17%.

– However Federal Government may, by notification in the official Gazette specify the taxable supplies in respect of which the further tax shall not be charged, levied and paid.

– SRO 648(1)/2013 dated 9th July, 2013 provides following list of persons on which this further tax @ 1% is not charged, levied or paid on the taxable supplies of:

(i) Electricity energy supplied to domestic and agricultural consumers.

(ii) Natural gas supplied to domestic consumers.

(iii) Motor oil, diesel oil, jet fuel, kerosene oil and fuel oil.

(iv) Goods sold by the retailers to end customers.

(v) Supply of goods directly to end customers including food, beverages, fertilizers and vehicles.

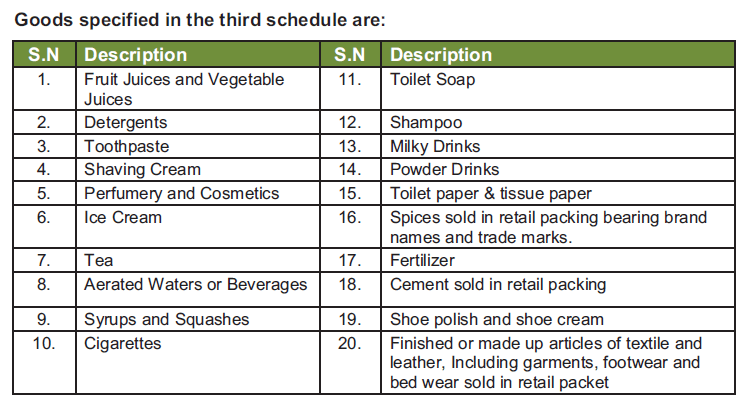

(vi) Items listed in Third Schedule to the Sales Tax Act, 1990.

Tax on taxable supplies specified in third schedule [Section 3(2)(a)]

– Sales Tax @17 % will be charged on the retail price on the goods specified in Third Schedule.

– The manufacturer shall legibly, prominently and indelibly print or emboss retail price along with the amount of sales tax on the packet, container, package, cover or label etc.

– Federal Government, may exclude from or include into said schedule any taxable supply by notification in the official Gazette.

Special rates of tax [Section 3(2)(b)]

The Federal Government is empowered to prescribe any higher or lower rate of tax in respect of any class of taxable goods.

Extra tax [Section 3(5)]

Federal Government is empowered to levy and collect tax at such extra rate or amount not exceeding 17% in addition to the amount of sales tax or retail tax, levied under Sales Tax Act, 1990. This tax shall be levied on the value of such goods or class of goods, on such persons or class of persons, in such mode, manner and at time and subject to such conditions & limitations as may be prescribed.

Capacity tax[Section 3(1B)]

Moreover the Board may levy and collect tax on the following instead of levying and collecting tax on taxable supplies:

a. production capacity of plants, machinery, undertaking, establishments or installations producing or manufacturing such goods; or

b. fixed basis, as it may deem fit, from any person who is in a position to collect such tax due to the nature of the business.

Tax on supply to CNG stations

– In case of supply of natural gas to CNG stations, the Gas Transmission and Distribution Company shall charge sales tax from the CNG stations at the rate of 17% on the value of supply to the CNG consumers.

– Value for the purpose of levy of sales tax shall include price of natural gas, charges, rents, commissions and all local, provincial and Federal duties and taxes but excluding the amount of sales tax

Special Powers to the Federal Government

The Federal Government or the Board is authorized to levy, in lieu of Sales Tax under section 3(1), by notification in the Official Gazette such amount of tax as it may deem fit on any supplies or class of supplies or any goods or class of goods. They are also authorized to specify the mode, manner or time of payment of such tax.

All PAC CFAP Mocks Winter 2016 Updated with solutions

Here is the related data for students appearing in ICAP CFAP Examination for Winter 2016.

SALES TAX

SALES TAX INTRODUCTION:

Here I would like to share with you the introduction to the sales tax laws applied in Pakistan.

Sales Tax Laws mainly include:

and some special rules include

Sales Tax Special Procedure Rules, 2007

Sales Tax Special Procedure (Withholding) Rules, 2007

Here are the useful notes on SALES TAX for better understanding of the above mentioned Laws.

TAXATION

Here we share the Video Lectures on Taxation Laws applicable in Pakistan.

Following is the List of Notes and Video Lectures;

1.2 Tax year as defined in ITO 2001

1.4- Scope of Income – Practice Questions

This material is equally useful for the understanding of the general public and more specifically my fellow students of Chartered Accountancy preparing for the following examination of Intermediate Stage CERTIFIED IN ACCOUNTING AND FINANCE (CAF) LEVEL and Final Stage CERTIFIED FINANCE AND ACCOUNTING PROFESSIONAL (CFAP) LEVEL under Institute of Chartered Accountants of Pakistan.

CAF 06 – PRINCIPLES OF TAXATION

CFAP 05 – ADVANCED TAXATION

This will provide basic knowledge in the understanding of objectives of taxation and core areas of Income Tax Ordinance, 2001, Income Tax Rules 2002 and Sales Tax Act 1990 and Sales Tax Rules.

Special Thanks to well known Chartered Accountant honorable Mr. Khalid Petiwal, a well-known Chartered Accountant, for such act of kindness.

Manufacturer-cum-Exporter

Sales Tax Act 1990

Section 2(17)

Manufacturer or producer [Section 2(17)]

Manufacturer means a person who engages, whether exclusively or not, in the production or manufacture of goods whether or not the raw material of which the goods are produced or manufactured are owned by him; and shall include:

⇒ a person who by any process or operation assembles, mixes, cuts, dilutes, bottles, packages, repackages or prepares goods by any other manner;

⇒ an assignee or trustee in bankruptcy, liquidator, executor, or curator or any manufacturer or producer and any person who disposes of his assets in any fiduciary capacity; and

⇒ any person, firm or company which owns, holds, claims or uses any patent, proprietary or other right to goods being manufactured, whether in his or its name, or on his or its behalf, as the case may be, whether or not such person, firm or company sells, distributes, consigns or otherwise disposes of

the goods.

Provided that for the purpose of refund under this Act, only such person shall be

treated as manufacturer-cum-exporter who owns or has his own manufacturing

facility to manufacture or produce the goods exported or to be exported;

Explanation:

The bare reading of the definition clarify that manufacturing services provided by a person on behalf of a principal are covered within the definition of manufacturing. For example dyeing services, toll manufacturing, knitting services etc.

Moreover, any person who either produces goods himself or out-sources

such manufacture is also treated as a manufacturer.

ICAP EDUCATION & TRAINING POLICY – 2013

Here is the ICAP Education and Training Policy 2013.

♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦

ICAP EDUCATION & TRAINING POLICY 2013

♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦♦

==========================================================================