WHAT IS THE SCOPE OF SALES TAX ?

It is very important question for a person studying SALES TAX ACT 1990, either for practice or for preparation of Examinations. Here we are going to share with you the scope of SALES TAX in Pakistan in nutshell.

Hope it will be helpful for you both in examinations and practice.

Normal rate of sales tax

– Sales tax @ 17% is charged, levied and paid on the value of:

(i) taxable supplies made by a registered person in the course or furtherance of any taxable activity carried on by him; and

(ii) goods imported into Pakistan.

– Where the taxable supplies are made to a person who has not obtained registration number, there shall be charged, levied and paid a further tax at the rate of 2% of the value in addition to the normal rate of 17%.

– However Federal Government may, by notification in the official Gazette specify the taxable supplies in respect of which the further tax shall not be charged, levied and paid.

– SRO 648(1)/2013 dated 9th July, 2013 provides following list of persons on which this further tax @ 1% is not charged, levied or paid on the taxable supplies of:

(i) Electricity energy supplied to domestic and agricultural consumers.

(ii) Natural gas supplied to domestic consumers.

(iii) Motor oil, diesel oil, jet fuel, kerosene oil and fuel oil.

(iv) Goods sold by the retailers to end customers.

(v) Supply of goods directly to end customers including food, beverages, fertilizers and vehicles.

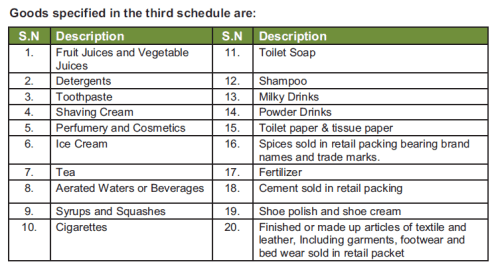

(vi) Items listed in Third Schedule to the Sales Tax Act, 1990.

Tax on taxable supplies specified in third schedule [Section 3(2)(a)]

– Sales Tax @17 % will be charged on the retail price on the goods specified in Third Schedule.

– The manufacturer shall legibly, prominently and indelibly print or emboss retail price along with the amount of sales tax on the packet, container, package, cover or label etc.

– Federal Government, may exclude from or include into said schedule any taxable supply by notification in the official Gazette.

Special rates of tax [Section 3(2)(b)]

The Federal Government is empowered to prescribe any higher or lower rate of tax in respect of any class of taxable goods.

Extra tax [Section 3(5)]

Federal Government is empowered to levy and collect tax at such extra rate or amount not exceeding 17% in addition to the amount of sales tax or retail tax, levied under Sales Tax Act, 1990. This tax shall be levied on the value of such goods or class of goods, on such persons or class of persons, in such mode, manner and at time and subject to such conditions & limitations as may be prescribed.

Capacity tax[Section 3(1B)]

Moreover the Board may levy and collect tax on the following instead of levying and collecting tax on taxable supplies:

a. production capacity of plants, machinery, undertaking, establishments or installations producing or manufacturing such goods; or

b. fixed basis, as it may deem fit, from any person who is in a position to collect such tax due to the nature of the business.

Tax on supply to CNG stations

– In case of supply of natural gas to CNG stations, the Gas Transmission and Distribution Company shall charge sales tax from the CNG stations at the rate of 17% on the value of supply to the CNG consumers.

– Value for the purpose of levy of sales tax shall include price of natural gas, charges, rents, commissions and all local, provincial and Federal duties and taxes but excluding the amount of sales tax

Special Powers to the Federal Government

The Federal Government or the Board is authorized to levy, in lieu of Sales Tax under section 3(1), by notification in the Official Gazette such amount of tax as it may deem fit on any supplies or class of supplies or any goods or class of goods. They are also authorized to specify the mode, manner or time of payment of such tax.